All companies listed on France’s CAC 40 stock market index have received several types of financial support (direct or indirect) during the health crisis. In addition to France’s short-term work compensation schemes, state-guaranteed loans and tax deferrals, other forms of support include a recovery and stimulus plan for several sectors (car industry, tourism, aviation, hydrogen...), the European Central Bank’s bond-buying program, capital provisions to protect so-called “strategic” firms, and a 20-billion euro cut in so-called ’production taxes’.

The government has pledged that this massive support would come with ’quid pro quos’ in terms of wealth-sharing, jobs and environmental protection. This report shows that none of these promises have been kept.

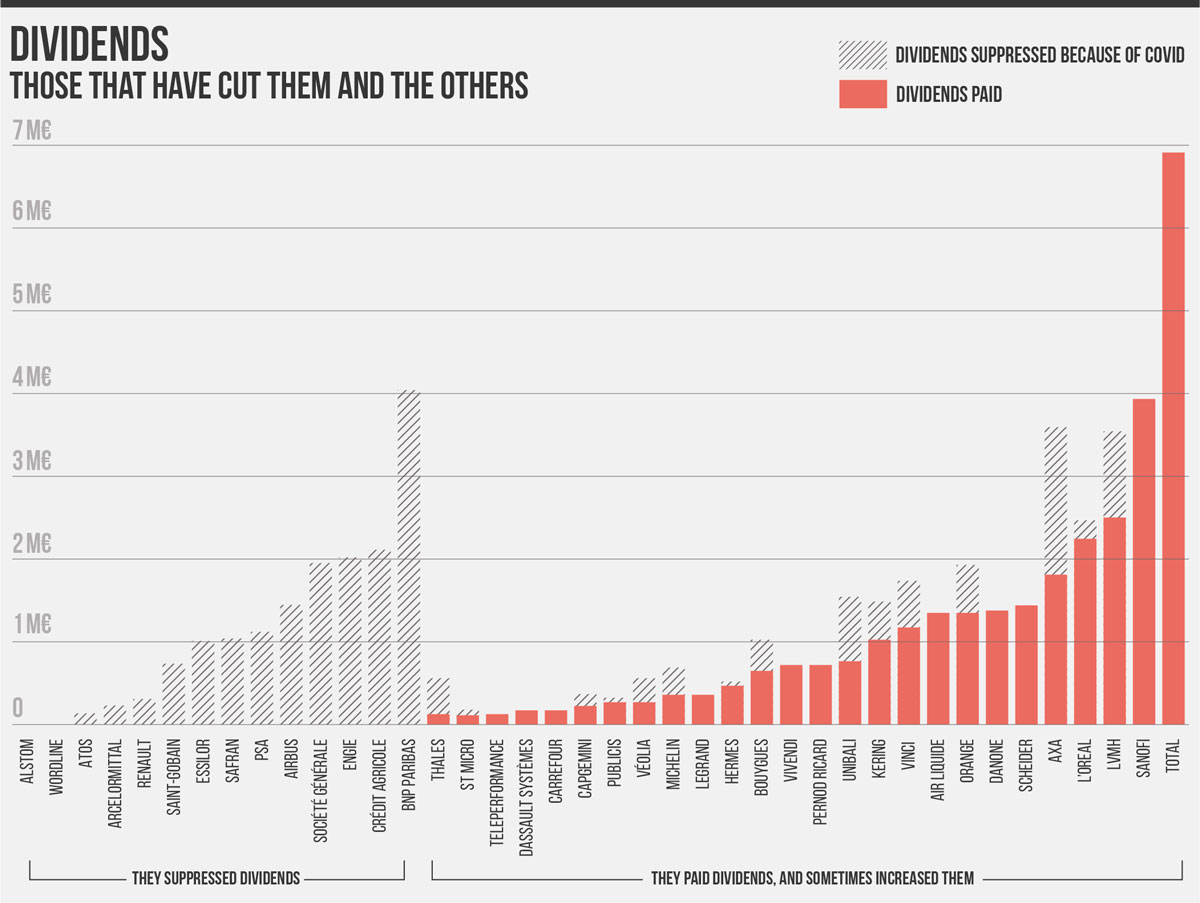

- Despite calls for “restraint” on dividend payments, many companies including Total, Sanofi and Danone have continued to pay out dividends while benefiting from indirect financial support. Barely a third of companies on the CAC 40 have actually suppressed dividend payments. In some cases, dividends were only reduced marginally. The dividend pay-outs of eight companies on the CAC 40 index were even up over last year.

- A third of companies on the CAC 40 index continued to pay out generous dividends while thousands of their employees were on the short-term work compensation schemes, with government funds used to pay their wages.

- Several companies, in which the French state holds shares, have disregarded the government’s commitments and continued dividend payments regardless.

- Major corporations that received direct or indirect public support, such as Renault, Airbus, Sanofi and Schneider Electric, have already announced tens of thousands of job cuts both in France and abroad.

- Companies have not had to make any effective commitments in terms of climate protection, and a significant number of their subsidiaries are still based in secret jurisdictions.

It should finally be highlighted that there is little transparency regarding state aid and subsidies to corporations. The public has almost no information on the actual figures or the amounts paid out, especially in regards to tax deferrals, the short-term work compensation scheme and extra capital invested in “strategic” companies.

We therefore recommend that:

- Direct and indirect state aid to companies be subject to binding conditions regarding climate, social and tax obligations. Compliance or failure to comply with these conditions must be verified by an independent agency and penalties should apply. Voluntary ’commitments’ and ’recommendations’ are clearly not enough.

- An independent public watchdog be set up which ensures transparency on state aid to companies, including all types of direct and indirect support, and compiles information on a company-by-company basis.

(click to enlarge)

Public funds poured into corporate heavyweights

In France, as elsewhere, the Covid-19 pandemic has prompted governments to dig deep into their wallets in order to revive the economy, save jobs and ensure businesses don’t go bankrupt. The figures are unprecedented and include almost 300 billion euros in loans, a 110-billion-euro emergency plan (including 7 billion to Air France and 5 billion to Renault), funds for the tourism industry, for the auto industry and for the aviation sector, tax cuts, support to reshoring, 100 billion euros for a stimulus plan, 31 billion for work compensation schemes, 76 billion in tax deferrals and waivers... Major corporations and their shareholders are taking most advantage of these measures despite their cash reserves and record dividend pay-outs over recent years.

Companies – and especially large corporations – are being showered with public funds. Even before the current health crisis, government financial support to businesses – so-called ’corporate welfare’ - represented 150 billion euros a year in France! The pandemic has only increased this support, and brought it into the limelight. It is no longer possible to shrug off the social and environmental conditions that should go hand in hand with it.

In addition to the obvious types of direct financial assistance, there are other forms of indirect support that companies like to keep under wraps. The European Central Bank’s bond-buying program is one such example [1]. There is a blatant lack of transparency around state aid, which both the French state and corporations seem eager to preserve, citing business confidentiality and tax secrecy. There is no way of knowing exactly which companies benefited from the short-time work compensation scheme, deferred taxes or deferred social security contributions, nor the amounts involved. Nor do we know what is done with the billions of euros injected into the Agence des participations de l’État (the French government shareholding agency) and public investment bank BpiFrance in order to protect so-called “strategic” companies from foreign predators, as the use of these funds is discretionary.

34 billion euros in dividends and share buybacks at the height of the health crisis

Corporations on the CAC40 should have announced a new record in dividend pay-outs at their annual general assemblies, most of which are held in May or June and coincided with the height of the pandemic, when France was in full lockdown: a historical 53.2 billion euros, excluding share repurchases. Aware that such astronomical figures would be frowned upon, public authorities and business groups called for restraint. After much procrastination, the French government agreed only to grant state-guaranteed loans or approve deferral of social security contributions to companies that did not pay out dividends nor repurchased shares. Companies could, however, still benefit from the short-term working compensation scheme and rely on support from central banks. AFEP, the CAC40’s lobby group, eventualy “recommended” that all its members make a 25% cut on dividend pay-outs.

These requests were heeded to varying degrees, with corporations on the CAC 40 index as well as all other major French companies taking a pick-and-choose approach. Barely a third of companies on the CAC 40 (13 firms) cancelled or suspended planned dividend payouts. Those that did were mostly major banks (BNP Paribas, Crédit agricole, Société générale) which were indirectly obliged to do so in order to be eligible for bank refinancing through the ECB, as well as large corporations that required government support in order to survive the health crisis (Airbus, PSA, Renault, Safran). Several of these companies have not ruled out dividend payments later in the year.

Two thirds of leading French corporations chose to either maintain dividend payouts or to reduce them, even when they received substantial direct or indirect support. The dividend payouts of eight companies were even up over the previous year: Teleperformance (+ 26.3%), Vivendi (+ 20%), Schneider Electric (+ 8.5%), Danone (+ 8.2%) , Dassault Systèmes (+ 7.7%), Total (+ 4.7%), Sanofi (+ 2.6%), Air Liquide (+ 1.9%). Bouygues, Hermès, Legrand and L’Oréal kept their dividends at the same level as last year (or decided against any increase).

Some “dividend cuts” were clearly just token gestures: in the case of Hermès, L’Oréal and Legrand, these were under 10%. And despite these cuts, L’Oréal and LVMH still managed to pay out over two billion euros to their shareholders, and Axa wasn’t far behind.

(click to enlarge)

Companies on the CAC 40 index will pay out 30.3 billion euros in dividends for the 2019 financial year – just over half of what was expected. Over the first half of 2020, share repurchases amounted to 3.7 billion euros (in addition to 11 billion euros for the 2019 financial year). This means that a total of 34 billion euros was paid out to shareholders at the height of the pandemic when the economy had come to a standstill.

Short-time work schemes: “nationalising wages as we have never done before”

In late March, Finance minister Bruno Le Maire’s asked companies to “behave decently: if you’re using the short-time work scheme, don’t pay out dividends”. This request, however, remained unheeded. The government then suddenly acted as though the short-time work compensation scheme was not state assistance designed to help companies but rather a “job-protection shield” that benefited employees and prevented redundancies. It thus ruled out introducing making it conditional to the suspension of dividend payouts.

This has meant that the French state has covered the short-time work of nearly 12.9 million employees from the corporate sector while many of these companies continued to pay out generous dividends. Laurent Burelle, chairman of Plastic Omnium and the influential leader of AFEP, the lobby group of CAC40, didn’t have any qualms about putting 90% of his employees on France’s short-time work scheme, while paying out a hefty dividend to the tune of 73 million euros, which both he and his close circle profited from.

With such flexible eligibility criteria, this was the first time France had seen so many employees on a short-time work scheme. It meant that the State and Unedic would pay a proportion of wages, capped at 4.5 times the minimum wage (approximately 4,800 euros net). Emmanuel Macron even spoke of “nationalising wages as we have never done before”, which enabled companies to retain trained and skilled employees at a reduced cost. 68% of large companies (over 500 employees), supposed to be fairly robust and often with substantial cash reserves, didn’t think twice about running to the French state for help [2].

At least 24 companies on the CAC 40 thus benefited from the short-term work scheme, and 14 of these payed out generous dividends (Bouygues, Capgemini, Carrefour, Kering, LVMH, Michelin, Publicis, Schneider, Teleperformance, Thales, Unibail, Veolia, Vinci and Vivendi). Outside of CAC40, the chemical company Solvay, which also signed up for the short-term work scheme, paid out 397 million euros in dividends.

Veolia, which paid out 284 million euros in dividends and is now ready to drop 10 billion euros to buy out its competitor Suez, used government funds to help pay 20,000 of its employees under the short-term work scheme. The call centre company Teleperformance (world leader in customer relationship outsourcing) also managed to pull off a 26.3% increase in dividend payouts while a portion of its employees were receiving barely decent wages under the short-term work scheme Several companies on the CAC 40 are being accused of taking illegal advantage of the scheme, including Bouygues’ construction subsidiary.

A pandemic of lay-offs

It is clear that the funds that corporations received from the French government are not being used to protects jobs.

Several days after government announced that it would be providing several billion euros in financial assistance to Renault as well as a rescue package for the automotive industry, the company announced that it would be cutting 15,000 jobs including 4,600 in France.

The French government also granted a seven-billion euro to Air France as well as announcing a recovery plan for the aviation sector. The company went on to announce 7,500 job cuts.

In June, Emmanuel Macron visited a Sanofi factory to announce measures to assist in reshoring the pharmaceutical industry. Several days later Sanofi announced 1,700 job cuts including 1000 in France.

Airbus, which will also benefit from the aviation recovery plan, is also planning on cutting 15,000 jobs worldwide, including 5,000 in France. And its subcontractors are following suit.

According to our figures, CAC 40 companies have announced nearly 60,000 job cuts in total, a quarter of which will affect French employees. And many of these job cuts are within companies such as Total, Sanofi and Schneider, which have chosen to continue dividend pay-outs.

Although the announcement of job cuts within these corporations is causing a stir, it is not necessarily the employees of these companies that will be most affected. It is the employees of these companies’ suppliers and subcontractors that, while attracting less attention, will bear the full brunt of both the direct consequences of the health crisis and those of the cost-cutting measures that corporations are implementing, resulting in less purchases and orders and more pressure to cut corners.

Many of the announced pandemic-related job cuts are not in fact due to the effects of Covid-19. France’s ’recovery plan’, announced in early September, includes 20 billion euros in tax relief for companies (in addition to the previously decided cut in corporate tax rates). It should be a priority right now that this support be subject to binding conditions in terms of job protection.

Green sheen

Much of the Covid support to business provided have benefited highly polluting companies and sectors, starting with the automotive industry (almost 5 billion euros paid out to Renault as well as 8 billion injected into the industry, and several billion under the recovery plan) and the aviation industry (a 7 billion-euro loan to Air France as well as measures under the aviation recovery plan). Even the oil group Total, one of the main companies fuelling the climate crisis, has benefited from indirect support through the cut on production taxes (which will primarily benefit climate-harming sectors) and the central banks’ bond-buying programme.

When the support measures for Air France and Renault were announced, a number of MPs and civil society organisations demanded that this support be subject to clear, ambitious environmental objectives. However, these were disregarded. The government had much to say about the climate “commitments” made by Renault and Air France in its reasoning for why there was no need to add unnecessary binding conditions to these. These “commitments”, however, either don’t exist or are based on “false solutions”, heavily subsidised by the French state, i.e, technologies that keep to the established industrial model as much as possible, thus ensuring the profits of transnational corporations are not disrupted – technologies, such as electric cars, which in fact do little in the way of climate protection.

Tax swindles

In addition to the ban on dividend payouts and share repurchases, the French government also stipulated that, in order to benefit from its support (guaranteed loans or tax deferrals), companies must not be based in tax havens.1 It seems indeed to make sense that companies should not benefit from state aid while at the same time avoiding paying their fair share of taxes.

And yet, once again, this turns out to more window dressing. The tax havens on the government’s official list only include a handful of tropical islands which are not used by French corporations, opting instead for European countries such as Luxembourg, Belgium and the Netherlands to dodge their tax obligations.

Maxime Combes and Olivier Petitjean