Albert Frère, Belgium’s wealthiest man, has just died at the age of ninety-two. As a key shareholder in Total, Engie, Lafarge and Pernod Ricard, he was tightly affiliated with the top French companies and with French politicians such as Nicolas Sarkozy. He cashed in on the Wallonia steel crisis in the seventies and eighties, profited from the sale of Belgium’s top companies to French transnational corporations and has been implicated in Lafarge’s involvement with Daesh in Syria. His career is a compendium of recent economic history: a tale of companies increasingly subjected to the demands of the financial world and to shareholders’ limitless greed, of governments doing away with industrial policies, and opening up the field to unscrupulous businessmen operating in a world where human rights and environmental concerns always come second in line to business interests.

Gresea (Research Group for an Alternative Economic Strategy), together with the Multinationals Observatory, has published a report [1] that highlights the shameful face behind the “master industrialist” celebrated today by the French and Belgian media. Groupe Bruxelles Lambert (GBL), the holding company owned by Albert Frère and the Quebec Desmarais family, was a key asset in building the Belgian businessman’s great fortune, a man whose net worth Forbes estimated to be at around five billion euros in 2017.

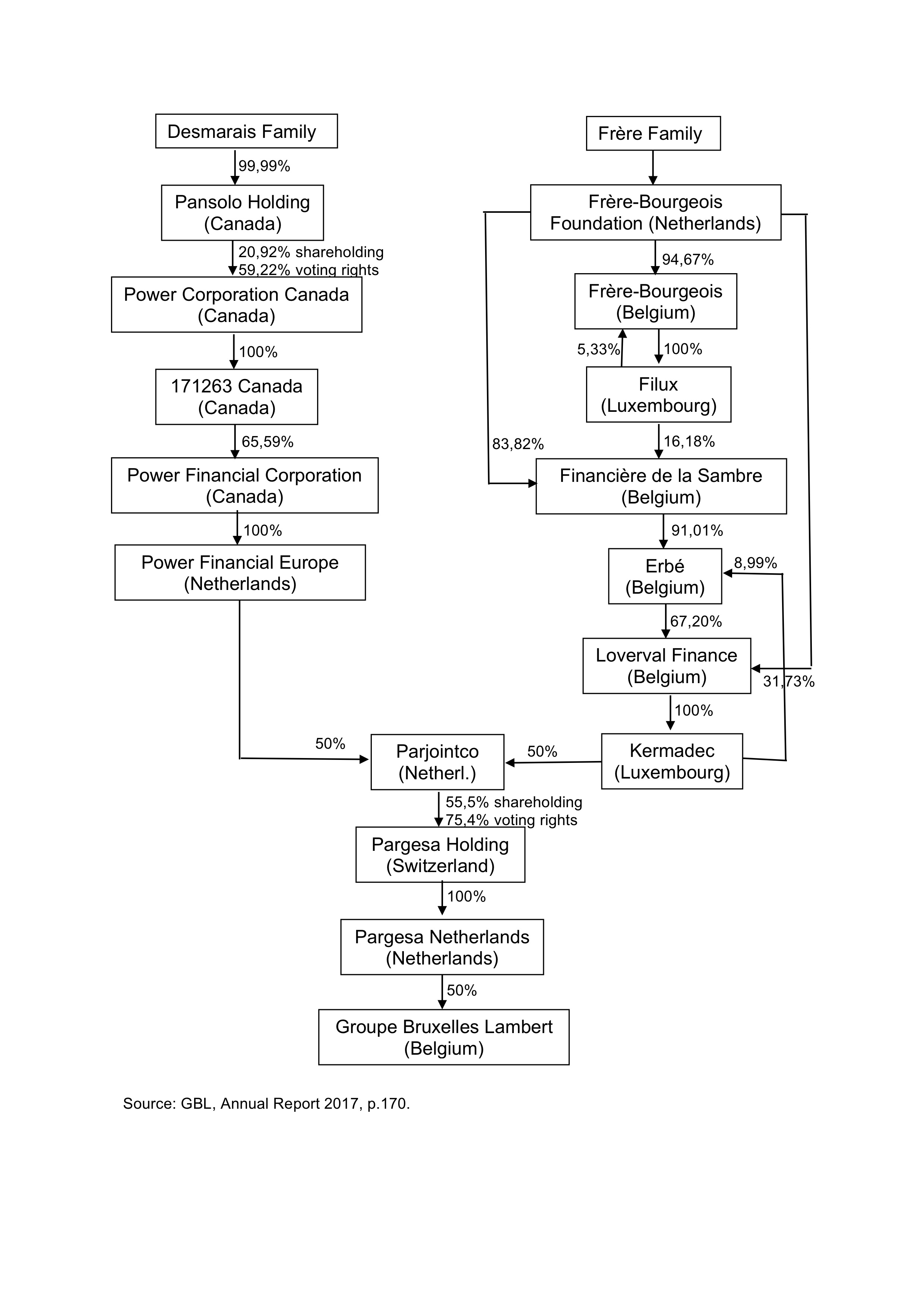

A nineteen billion dollar holding company hiding in the shadows of the CAC40 heavyweights

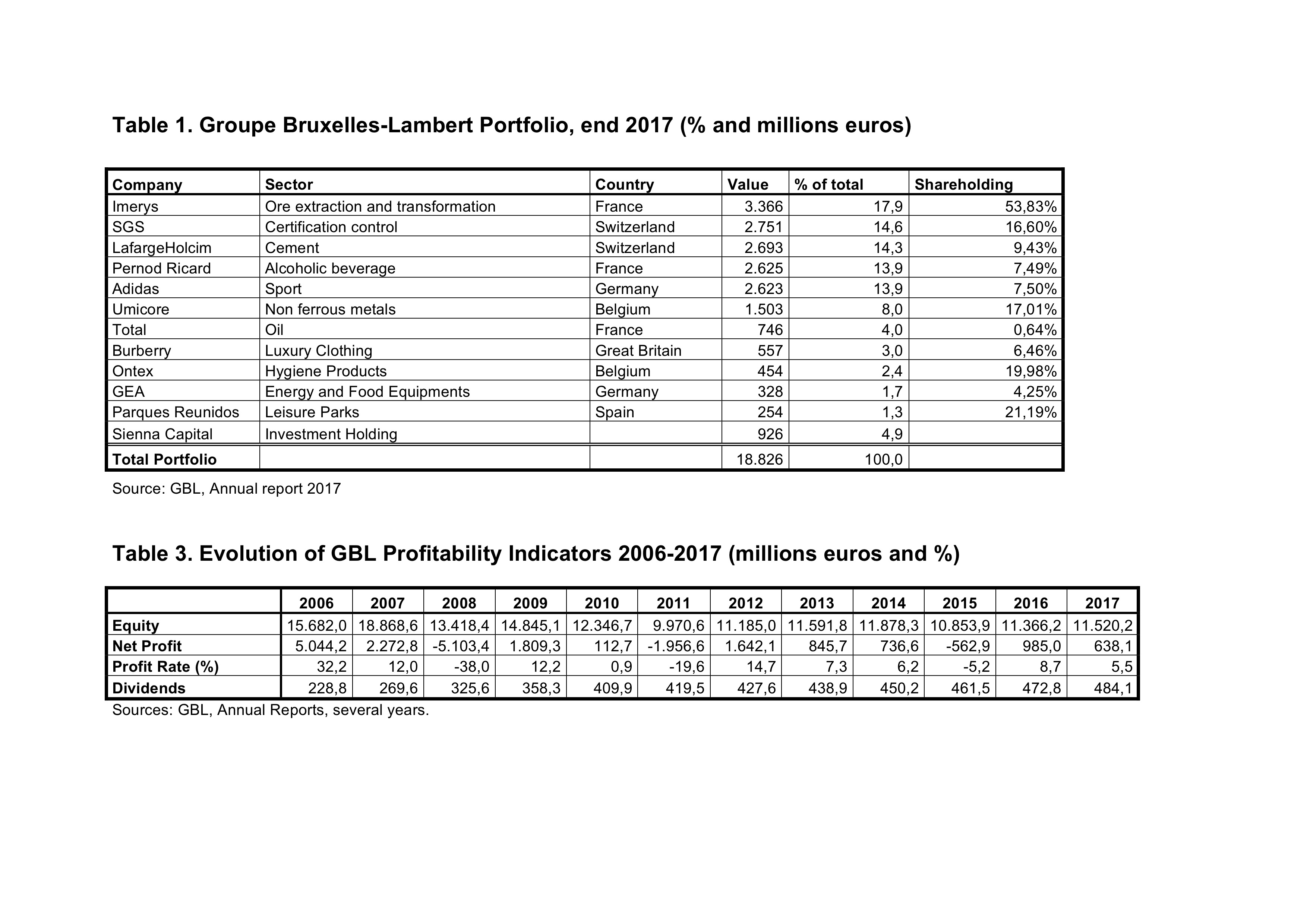

Never heard of Groupe Bruxelles Lambert? Although it boasts a portfolio evaluated at nineteen billion euros, the company remains relatively unknown. And yet any story about job cuts, measly salaries, generous dividend pay-outs, environmental crimes, corruption scandals on the other side of the world involving transnational corporations such as Total, Lafarge, Pernod Ricard and Adidas, is also in a way a story about GBL. It is one of those holding companies through which wealthy families hold majority shares in a number of corporations, playing a key role in influencing these companies’ corporate strategies and decisions. These holding companies often operate by stockpiling companies located in Belgium Switzerland, Luxembourg and the Netherlands, which has the dual benefit of reducing their tax bill and enabling them to increase their investment capacity by making the capital of these companies available to minority shareholders while they retain control. This is exactly what GBL did. By putting a chunk of their assets in GBL, Albert Frère and his family found themselves sitting, with the Desmarais family, on a nineteen billion dollar portfolio.

It’s not easy to pinpoint a consistent industrial strategy behind Groupe Bruxelles Lambert’s current holdings which range from cement (LafargeHolcim) to sports and fashion (Adidas, Burberry), as well as alcoholic beverages (Pernod Ricard), oil (Total), ore extraction and processing (Imerys, Umicore), inspection and verification (SGS), disposable hygiene products (Ontex), amusement parks (Parques reunidos), agri-food technology (GEA) and finance (Sienna Capital). Albert Frère’s family also directly owns a 0.6% share of Total as well as of another smaller holding company: the Compagnie nationale à portefeuille (CNP), which owns 7.2% of shares in French television M6, as well as a company implicated in unconventional gas projects in former coal mines in Belgium and Northern France.

Pumping out dividends…

The only distinguishable constant between all GBL’s investments is quite simply the priority made to paying out shareholders. GBL received 461 million euros in dividends in 2017, the majority of which came from LafargeHolcim, SGS and Imerys. Despite fluctuating profit margins over the years, dividends paid out by GBL to Albert Frère and his family have steadily increased, jumping from 229 million euros in 2006 to 484 million in 2017 (see the table below). Between 2010 and 2015, after the ripples of the financial crisis, GBL’s profit climbed to just 818 million euros, but the holding company dished out no less than 2.6 billion euros in dividends to its wealthy shareholders.

Firms under the holding company’s control often took a similar approach in their business dealings. Engie’s (previously GDF Suez) tendency to pay out huge dividends despite financial losses has been the subject of much criticism. Between 2009 and 2017, the company paid out over 29 billion euros to its shareholders, three times more than its profits over the same period (9.7 billion). In 2013 and 2015, Engie even paid out substantial dividends despite a loss of several billion euros. It’s hard not to put two and two together given the fact that GBL was at this time one of the utility company’s main shareholders, along with the French government, which validated this strategy.

Two years ago Albert Frère and GBL sold their shares in the French utility company that helped build their fortune. They also reduced their shares in Total. GBL’s portfolio has been radically restructured, with 14 billion euros in sales and acquisitions since 2012. According to Gresea, this is a sign that it had decided to forego industrial purpose and were operating according to a purely financial logic: “No longer was there any interest in creating an empire; the only concern was building a structure that could rake in as much money as possible.” In 2015, the patriarch stepped down from the group’s operational management, handing over the reins to his son-in-law Ian Gallienne and his loyal friend Gérard Lamarche.

From the nails shop to the nobility

Although Albert Frère was given the title of Baron by the Belgian King in 1994 and is now celebrated in his native country, he was for a long time looked down upon by the country’s ruling elites. The Belgian aristocracy saw Frère as just a petty “nails dealer” due to the fact that he began his career by taking over his parents’ nails and chains factory in Charleroi, just after the Second World War. The key moment in his rise to riches was in 1982 with the acquisition of the Groupe Bruxelles Lambert – a prestigious finance company that had been around since the nineteenth century and that had stakes in a number of Belgian companies.

At the turn of the seventies and eighties, Albert Frère indeed managed to capitalize on the situation for his own personal gain, particularly the declining Wallonia steel industry where he carved out an increasingly important place for himself. His virtual monopoly on steel sales, automatically receiving a commission for every ton sold, meant that he could be sure of an easy profit, despite the fact that the sector was collapsing. There were thousands of job cuts in the steel industry between the seventies and nineties. The Belgian government had to intervene and invested a substantial amount in restructuring the sector. And when the government sought to take back control of steel sales, Albert Frère set a high price: two billion Belgian francs – what those on the inside of GBL were to call “the dowry” – the initial sum that would enable the businessman to launch into other acquisitions.

In 1981, socialists’ came to power in France - another factor that was to help the businessman on his way. The French bank Paribas, at risk of being nationalised, contacted Albert Frère, with whom it had a long partnership, requesting him to protect some of its assets. Frère’s solution was to put these assets in subsidiaries based in Switzerland and Belgium, with the condition that Paribas would hand over 51% of shares to trusted partners such as Albert Frère and Paul Desmarais, (this was to constitute their first business partnership). Bolstered by the cash influx and the relationships that went along with it, Albert Frère then came to the rescue of Groupe Bruxelles Lambert, recapitalising it and gradually taking control of it as well as many of Belgium’s top companies.

Belgium’s prized companies sold to French TNCs

Electrabel was sold to GDF Suez (now Engie), Petrofina went to Total, the insurance company Royale Belge haggled off to Axa, Fortis laid on a platter to BNP Paribas, the GIB supermarket group sold to Promodès before it merged with Carrefour, the BBL bank entrusted to its Dutch competitor ING ... Albert Frère’s subsequent career is not much more than a string of Belgian heavyweights sold off to foreign (primarily French) corporations, in exchange for a percentage of the capital in these companies. This is precisely how a “nail dealer” became one of the largest shareholders of Total and GDF Suez. This was to be a tactic he would use again, but this time France would be on the losing end with the merger between Lafarge and Swiss competitor Holcim.

The career of the Charleroi businessman is tightly entwined with the French business elite, first very early on with Paribas, before the company became BNP Paribas, and then later with Suez, joining forces with the company in the eighties against Italian businessman Carlo de Benedetti, to take control of the prestigious bank and holdings company SGB (Société générale de Belgique) and its key asset: Electrabel, which then had a virtual monopoly on Belgium’s electricity in market, and owns several ageing nuclear power plants.

Albert Frère was also closely aligned with LVMH and its chair and CEO Bernard Arnault. In 1998, they took over Château Cheval Blanc, a winery located in Saint-Émilion in Gironde. Albert Frère had served as director of LVMH since 1997, but in 2017 gave up the position, taking over the role of advisory board member. His daughter Ségolène Gallienne is a director of Christian Dior, LVMH’s parent company. Bernard Arnault serves as director at Frère-Bourgeois.

Economic advisor to the former French President

As Nicolas Sarkozy’s main economic advisor, Albert Frère was also in league with the political world, and the former French President awarded him the Legion of Honour’s Grande Croix as soon as he was sworn in. While Sarkozy was still Minister of the Economy, Frère was accused of benefiting from unexplained indulgence from the Caisse des dépôts et consignations. This state-owned financial institution purchased his shares in the BTP Eiffage construction group and the Quick fast-food chain at an abnormally high price, enabling him to bolster his capital in Suez just before the company merged with GDF. A businessman who had fallen out with Frère filed a complaint with the French and Belgian courts but these were deemed inadmissible.

This was not the only stain on Albert Frere and his group’s reputation. In the late eighties, GBL mysteriously escaped prosecution following the resounding bankruptcy of Wall Street bank Drexel Burnham Lambert, of which it was one of the key shareholders. More recently, another company controlled by Albert Frère was complicit in corruption scandals involving Brazil’s state oil company Petrobras [2]. In 2008, the latter had effectively agreed to buy a refinery in Texas from Albert Frère for 800 million dollars – nearly twenty times more than what the Belgian businessman had paid to acquire it only three years earlier. … Albert Frère and Paul Desmarais’s networks also appear to have played a role in the UraMin affair, the Canadian mining company with worthless assets, which Areva paid an astronomical price for in the 2000s [3].

Frère’s implication in the civil war in Syria and the destruction of the Amazon Rainforest

The most disturbing scandal, however, may be the latest one – that of Lafarge’s cement factory in Syria. There has been much criticism of Lafarge’s directors, who insisted on keeping their cement factory in Syria open despite the civil war raging in the country, and who, in exchange, agreed to pay out several million euros to various armed groups including Daesh. The executives involved, who include former CEO Bruno Lafont, are currently under formal investigation, as is Lafarge as a legal entity. But what about the liability of shareholders like Albert Frère and Nassef Sawiris, sitting on the company’s board of directors, and who, it is rumoured, went to great lengths, along with Holcim’s shareholders, to pin all liability onto Lafarge’s French executives? It would be hard to believe that they were unaware of what was going on in Syria. And it appears that their insistence on keeping the cement factory in Jalabiya open was purely for financial reasons: there were, of course, the company’s profits to think about, but they also wanted to avoid depreciating assets as Lafarge was heavily indebted and ecould nd up in a situation where its creditors would demand early repayment. There were enough murky details to incite the Belgian police to wiretap several of GBL’s directors including Albert Frère and his son Gérald [4]. The investigation is currently underway.

The Lafarge case revealed another grey area in Albert Frère’s legacy: the number of human rights abuses and environmental crimes that have occurred in his increasingly internationalised business affairs. The Lafarge case in Syria is not a one-off, as illustrated by an article published by Le Monde, which raised questions about the activities of Imerys (another firm owned by GBL) on the border of Afghanistan and Pakistan, where it appears it indirectly contributed to financing the Taliban [5].

The Multinationals Observatory recently revealed how this same company was involved in spreading and fuelling social violence in communities living around the Amazon Rainforest [6]. GBL was already one of those orchestrating Engie’s (then GDF Suez) massive investment in Brazil’s energy sector, particularly through the construction of the Jirau mega-dam in the Amazon basin, a money pit that has resulted in countless social and environmental problems (see the case study on Jirau published alongside this one).

And it appears there is the same mentality when it comes to workers’ rights: two successive reports published by the organisations Éthique sur l’étiquette and Basic have illustrated how Adidas, another of GBL’s nest eggs, as well as Nike, choose to prioritise shareholders and advertising over their workers who make their products in Asia and are paid next to nothing [7].

There is growing awareness of the liability of transnational corporations that, so far, generally manage to get away with their misdeeds by dodging national jurisdictions. In 2017, France adopted a corporate “duty of vigilance” law whereby corporations are legally required to prevent serious human rights abuses and environmental harm caused by their activities. A treaty along the same lines is currently under negotiation at the United Nations, in spite of the more or less blatant resistance expressed by the business community and the western world. If there are any last lessons to be drawn from Albert Frère’s career, it would have to be that the law needs to go even further than holding companies and their directors to account; it needs to pull back the curtains and expose those who are pulling the strings.

| Albert Frère Country : Belgium Net Worth : 5 billion € in 2018 (Forbes.) = more than 128,000 years of the Belgian average wage = more than 313,000 years of the Spanish average wage Sector : Steel, Energy, Investments Companies : Groupe Bruxelles Lambert, LafargeHolcim |

{kind=link}

{kind=link}